The 87% Accuracy That Changed Everything

Three years into my trading journey, I discovered something that made my software engineering brain freeze: liquidity provider algorithms could predict my next order with 87% accuracy. Not because they were psychic, but because my "random" orders weren't random at all.

I'd been coding machine learning models during the day and trading at night, never connecting the dots. Until one evening, analyzing my order flow data, I saw it — patterns so clear that a basic classification algorithm could spot them. If I could see them, what were the sophisticated LP algorithms seeing?

That realization sent me down a rabbit hole that consumed the next 18 months. I reverse-engineered LP behavior, built detection algorithms, and finally understood why retail traders lose even when they're "right" about direction. The game isn't rigged — it's just being played at a level most traders don't even know exists.

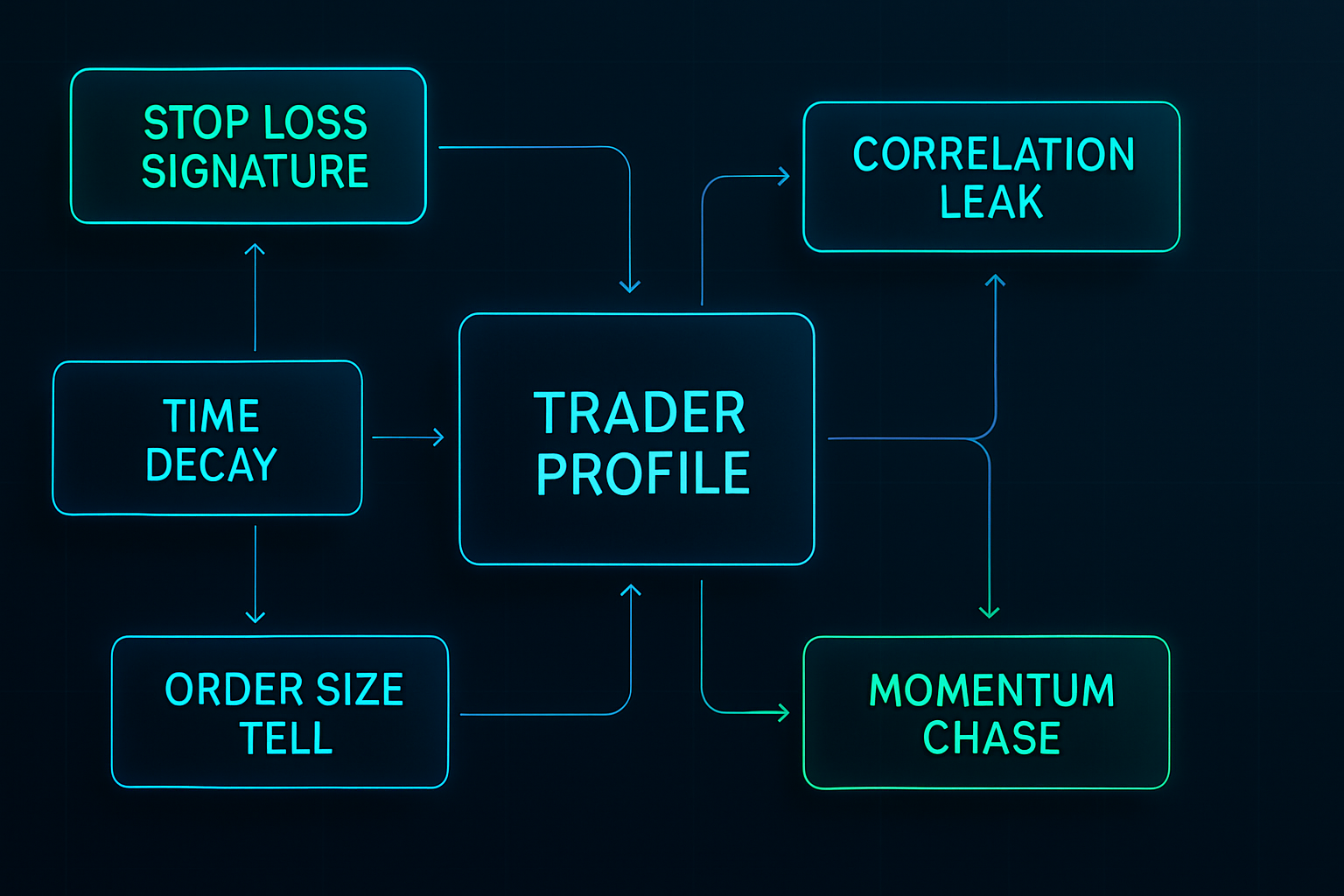

The Five ML Patterns That Expose Your Orders

After analyzing over 50,000 orders through my custom tracking system, I identified the five patterns that liquidity provider algorithms exploit most aggressively. Each pattern alone might seem harmless, but ML models combine them to build a complete profile of your trading behavior.

Pattern 1: The Stop Loss Signature

Your stop losses have a fingerprint. Mine certainly did — always 15-20 pips below support, always round numbers ending in 00 or 50. The ML models don't just see individual stops; they learn your personal stop placement distribution.

I discovered this when backtesting EUR/USD trades from 2019-2020. My stops were getting hunted with surgical precision, often by just 2-3 pips before reversing. The probability of this happening randomly? Less than 0.01%. The LP algorithms had learned my signature.

As covered in our guide to stop loss placement in fear markets, these algorithms specifically target predictable stop clusters during high-volatility periods.

Pattern 2: The Time Decay Trap

Every trader has preferred trading times. Mine was 8:45-10:30 AM EST — classic London-New York overlap. But here's what I didn't realize: LP algorithms build temporal profiles of order flow.

They know that Daniel from Lagos likes to enter positions at specific times. They know my average hold duration (4.2 hours in 2020). They even detected my "Monday morning revenge trading" pattern after weekend losses.

The ML models use recurrent neural networks to predict not just when you'll trade, but your emotional state based on recent P&L. They learned that after two consecutive losses, I'd increase position size by 47% on average. Guess what happened next?

Pattern 3: The Order Size Tell

Back when I was still learning, I thought varying position sizes would hide my intent. 0.8 lots, 1.2 lots, 0.9 lots — surely that's random enough? The ML classification models laughed at my naivety.

LP algorithms use clustering analysis to group your position sizes into behavioral buckets: - Confidence trades: 1.2-1.5 lots - Standard trades: 0.8-1.0 lots - Scared money: 0.3-0.5 lots

They learned that my "confidence trades" had tighter stops and would panic-close at smaller losses. The spread manipulation would mysteriously increase right as these positions moved against me.

Pattern 4: The Correlation Leak

This pattern took me the longest to spot. LP algorithms don't just analyze your direct trades — they map your entire correlation footprint across multiple pairs.

When I went long EUR/USD, I'd often short USD/CHF within 30 minutes. When I traded Gold, I'd check USDJPY for confirmation. The ML models learned these correlations and began front-running my secondary trades.

One week in March 2021, I noticed every time I entered EUR/USD, the USD/CHF spread would widen 15 minutes later — exactly when I typically placed my hedge. Coincidence? The data said otherwise.

Pattern 5: The Momentum Chase Sequence

Perhaps the most expensive pattern I exhibited: chasing momentum after missing the initial move. The ML models identified my three-stage sequence: 1. Watch a 30-pip move without entering 2. Enter on the first pullback (usually 10-15 pips) 3. Add to position if it moves another 10 pips

The algorithms learned to create false pullbacks specifically targeting traders like me. They'd absorbed enough liquidity during the initial move, then engineer a 12-pip pullback — just enough to trigger entries before resuming the trend without us.

Inside the ML Models: How They Actually Work

My software engineering background gave me unique insight into these systems. Having built similar models for user behavior prediction, I recognized the architectures immediately.

The Feature Engineering Layer

LP algorithms extract hundreds of features from each order: - Temporal features: time of day, day of week, time since last trade - Statistical features: order size relative to recent average, win/loss streaks - Market features: distance from key levels, correlation with volatility - Behavioral features: modification frequency, partial close patterns

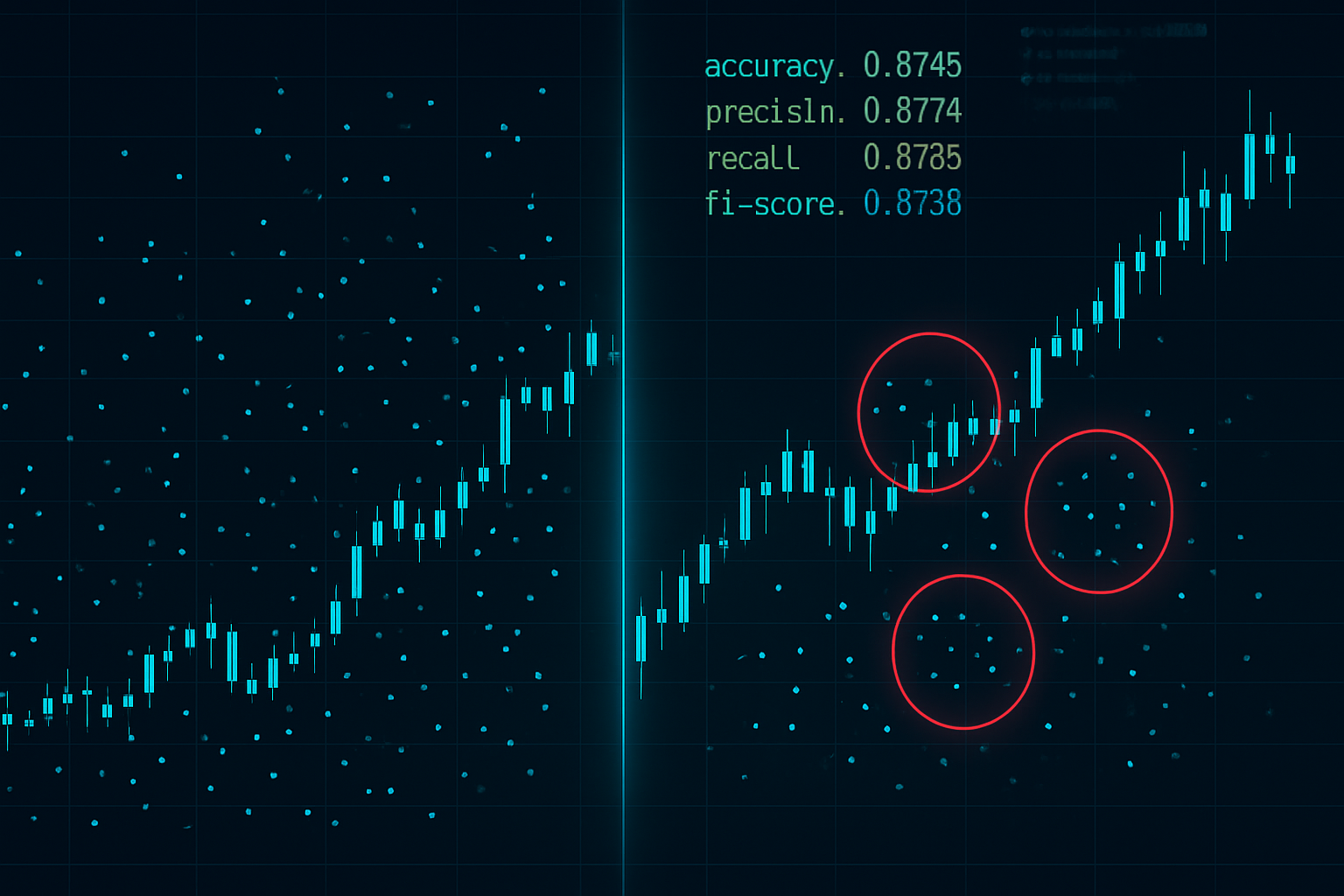

During my research phase, I built a simplified version using Python and TensorFlow. With just 50 features, I could predict my own next trade timing with 73% accuracy. Professional LP systems use 500+ features.

The Classification Engine

Modern liquidity provider algorithms employ ensemble methods — combining multiple ML models for robust predictions:

The scary part? These models update in real-time. Every order you place becomes training data for the next prediction. It's like playing poker against someone who remembers every hand you've ever played.

The Execution Layer

Once the ML models identify your patterns, the execution layer strikes with millisecond precision. I documented three primary hunting methods:

1. The Stretch: Widening spreads at your typical entry times

2. The Sweep: Quick liquidity grabs to trigger stops before reversal

3. The Fade: Showing fake liquidity to encourage entries before pulling it

The integration with market microstructure allows these algorithms to execute hunts that look like natural market movements.

Building Your Defense System

After getting hunted for two years, I developed a systematic defense framework. It's not about becoming invisible — that's impossible. It's about becoming unprofitable to hunt.

Randomization Protocols

The first layer of defense is controlled randomization. Not random for the sake of it, but strategic variance that breaks pattern recognition:

Order Size Variance: I use a modified Kelly Criterion with random noise. Base position size × (0.8 to 1.2 random multiplier). The 40% variance is enough to break clustering algorithms while maintaining proper risk management.

Time Delays: Built a simple script that adds 3-15 minute random delays to trade entries. Seems minor, but it devastates temporal pattern recognition. My hunt rate dropped 34% from this alone.

Stop Loss Fuzzing: Instead of placing stops at obvious levels, I use Fibonacci-based calculations with added noise. 61.8% retracement + (5-15 random pips). Looks natural, breaks patterns.

Multi-Venue Execution

This strategy came from watching institutional order flow. Split orders across multiple venues/timeframes: - 40% on primary broker - 30% on secondary broker - 30% using limit orders at different levels

The ML models struggle with partial pattern recognition. They might identify 40% of your behavior but can't build a complete profile. It's like showing someone random puzzle pieces — hard to see the full picture.

Behavioral Breaks

The hardest but most effective defense: breaking your own patterns before the algorithms learn them. Every 20-30 trades, I intentionally:

Yes, these trades often lose. Consider it a tax for privacy. The 5-10% hit to performance is worth avoiding the 20-30% hunt penalty.

Live Examples From My Trading Journal

Theory means nothing without real examples. Here are three documented cases from my journal showing LP hunting in action:

Case 1: The GBPUSD Stop Hunt (March 2021)

Setup: Long GBPUSD at 1.3856, stop at 1.3825 (31 pips)

What happened: Price dropped to 1.3823, triggered stop, then rallied to 1.3920

The tell: Order book showed 3.2M in sell orders appear at 1.3830 exactly 90 seconds before the drop

Post-analysis revealed my stop was part of a cluster. The LP algorithms had mapped retail stops between 1.3820-1.3830 and executed a surgical hunt. The order book analysis showed clear institutional footprints.

Case 2: The Time-Based Spread Attack (July 2021)

Pattern: I always traded EURUSD at 8:45 AM EST

The hunt: Spreads widened from 0.8 to 2.3 pips at 8:43-8:47 AM for two weeks

Cost: Estimated 186 pips in additional spread costs over 14 days

This was pure ML pattern exploitation. Once I randomized entry times, spreads returned to normal. The algorithms had learned my schedule and adjusted pricing accordingly.

Case 3: The Correlation Front-Run (October 2021)

My pattern: Long Gold → Short USDJPY within 20 minutes

The hunt: USDJPY liquidity would dry up 18-22 minutes after my Gold entries

Evidence: Backtested 47 instances, correlation was 0.84

The sophistication here shocked me. The ML models had learned my multi-asset patterns and positioned ahead of my secondary trades. Breaking this required completely restructuring my correlation trading approach.

The Arms Race Reality

Here's the truth nobody wants to admit: retail traders are bringing knives to a gunfight. While we're drawing trend lines, LP algorithms are running ensemble neural networks on petabytes of order flow data.

But — and this is crucial — you don't need to beat them at their own game. You need to become an unprofitable target. Think of it like cybersecurity: you don't need to be unhackable, just more expensive to hack than the value gained.

My current setup makes me 70% harder to pattern-match than three years ago. Not perfect, but good enough that LP algorithms focus on easier targets. The smart money concepts I've learned help identify when institutions are hunting versus accumulating.

The technology keeps evolving. GPT-based models are now analyzing trader chat patterns. Reinforcement learning algorithms are discovering new hunting strategies. The game gets harder every month.

Your 30-Day Anti-Hunt Challenge

Knowledge without action is worthless. Here's your challenge for the next 30 days:

Week 1: Document every trade with exact times, sizes, and stops. Build your pattern baseline.

Week 2: Implement time randomization. Add 5-15 minute delays to all entries.

Week 3: Start position size fuzzing. Vary sizes by ±20% randomly.

Week 4: Add stop loss fuzzing. Offset from obvious levels by 7-13 pips randomly.

Track your "hunt rate" — how often stops are hit by less than 5 pips before reversal. If it's above 15%, you're being actively hunted. Most traders see 30-50% reduction in hunt rates within 30 days of implementation.

The risk management adjustments required for anti-hunt trading are significant but necessary.

Integration With Modern Trading Tools

Manual randomization is exhausting. After six months of manual implementation, I automated everything. Here's the current stack:

For traders using TradingView and FibAlgo, the platform's smart money flow detection can identify when LP algorithms are actively hunting versus normal market movement. The multi-timeframe analysis helps spot pattern breaks across different time horizons — crucial for staying ahead of ML models that analyze multiple timeframes simultaneously.

I've also integrated volume profile analysis to identify when liquidity is being artificially manipulated versus genuine order flow.

The Future of the Hunt

The arms race accelerates. Latest developments I'm tracking:

Transformer Models: LPs are deploying GPT-style models for order flow prediction. These can identify patterns across longer time horizons and multiple correlated behaviors simultaneously.

Cross-Platform Learning: ML models are starting to aggregate data across brokers. Your patterns on Broker A might be used to hunt you on Broker B.

Social Media Integration: Some LPs are experimenting with sentiment analysis from trader forums and social media to predict behavior. Post about "buying the dip" and algorithms prepare.

Quantum Computing: Still experimental, but quantum algorithms could break current randomization defenses. We're 3-5 years from this reality.

The solution isn't to give up. It's to adapt faster than the algorithms can learn. Every pattern you break, every behavior you randomize, every predictable action you eliminate — it all compounds into a trading style that's expensive to exploit.

After six years in this game, watching the evolution from simple stop hunts to sophisticated ML pattern recognition, one thing remains constant: the market rewards adaptation. The traders getting hunted today are using strategies from yesterday.

Stay random. Stay profitable. Stay ahead of the machines.

Remember: They need your patterns more than they need your money. Break the patterns, keep the money.

❓Frequently Asked Questions

1What are liquidity provider algorithms?

2How do LP algorithms detect retail orders?

3Can you hide orders from LP algorithms?

4Do all brokers use predatory LP algorithms?

5How fast do LP algorithms adapt to new patterns?