The Day Rate Derivatives Printed 523% While Equities Burned

Every trader remembers where they were on March 15, 2020. The Fed just slashed rates to zero. Equity traders were getting massacred. Currency pairs were going haywire. But on the JPMorgan rates desk next to ours, something extraordinary was happening. A single Eurodollar option position had just turned £50,000 into £311,500 in 48 hours.

That's when I learned the truth about volatility trading during fear spikes. While everyone fixates on VIX calls or equity puts during crashes, the real money hides in interest rate derivatives. When central banks panic, rate markets go nuclear.

After 14 years trading FX at JPMorgan and watching rate traders during every major policy shift, I've seen this pattern repeat: Fear markets create the most violent repricing in rate expectations. And if you know which contracts to trade, the leverage is astronomical.

Why Rate Derivatives Explode When Fear Strikes

Here's what retail misses: Interest rate derivatives aren't about betting on rates going up or down. They're about betting on the speed and magnitude of central bank response to fear.

When fear hits, the market rapidly reprices rate expectations. In March 2020, the market went from pricing zero rate cuts to pricing 150 basis points of cuts in 72 hours. That violent repricing creates astronomical moves in rate derivatives.

Consider the mathematics. A 2-year Treasury future moves roughly $2,000 per basis point per contract. When the market reprices 100 basis points of rate cuts, that's a $200,000 move per contract. With futures margin at $3,000, you're looking at 66:1 effective leverage.

But here's where it gets interesting. Options on those futures can provide 10x additional leverage. During the COVID crash, certain Eurodollar call options moved from $250 to $15,000 per contract. That's 60x in five trading days.

The key is understanding how institutions position during fear markets. Banks don't buy VIX calls. They buy rate optionality.

Trade #1: The Brexit Butterfly (June 2016)

Let me walk you through three actual trades that demonstrate this principle. First, Brexit.

On June 20, 2016, with polls showing Remain ahead, I noticed something odd. Short Sterling futures were pricing almost zero chance of a Bank of England rate cut. But the options skew told a different story. Deep out-of-the-money puts were bid aggressively.

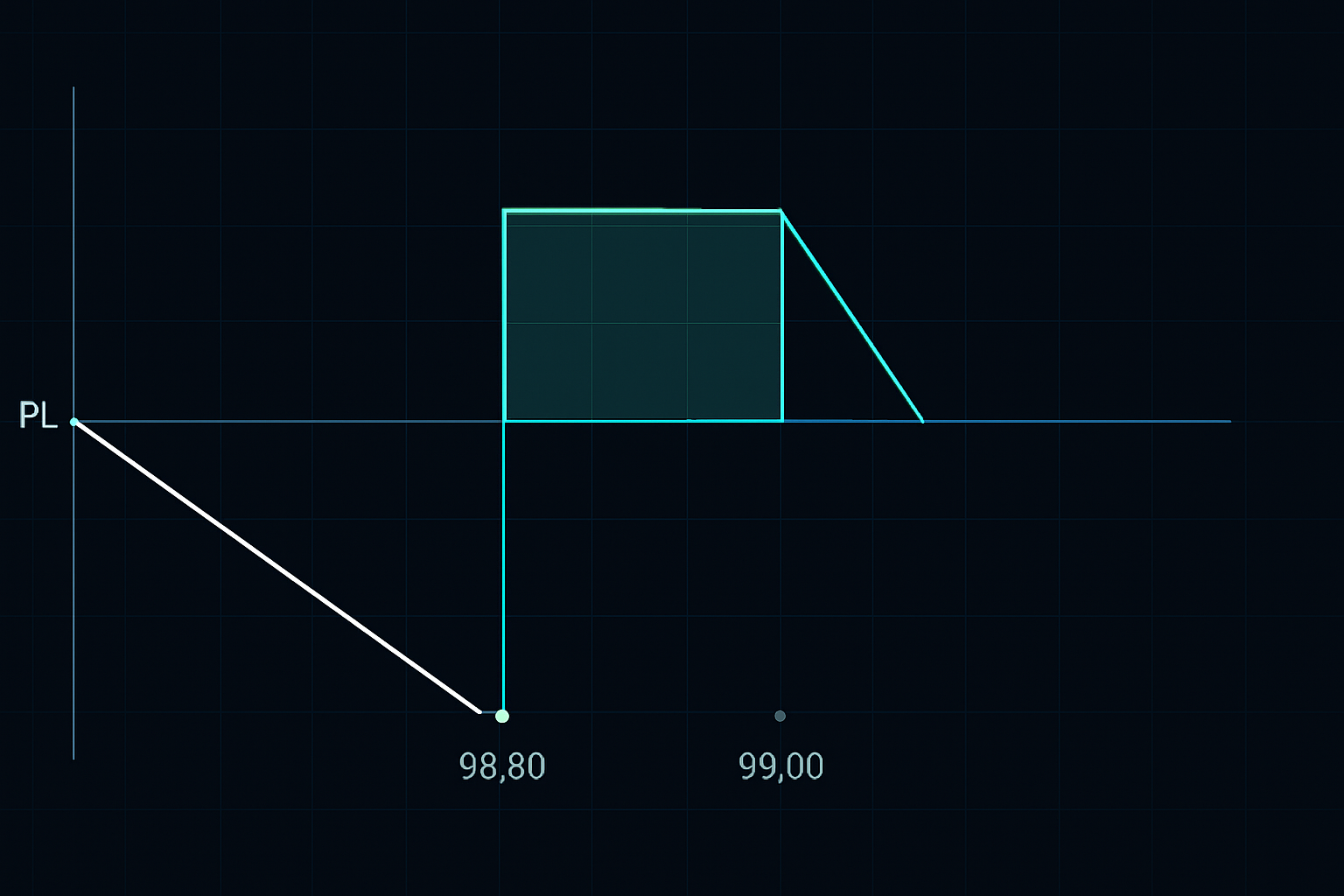

The setup: Short Sterling butterfly spread

- Buy 1x Sep16 99.25 put at 8 ticks

- Sell 2x Sep16 99.00 puts at 22 ticks each

- Buy 1x Sep16 98.75 put at 48 ticks

- Net credit: 12 ticks ($300 per spread)

Maximum profit if futures settled exactly at 99.00: 25 ticks ($625). Maximum loss: 13 ticks ($325). Risk/reward: 1.9:1.

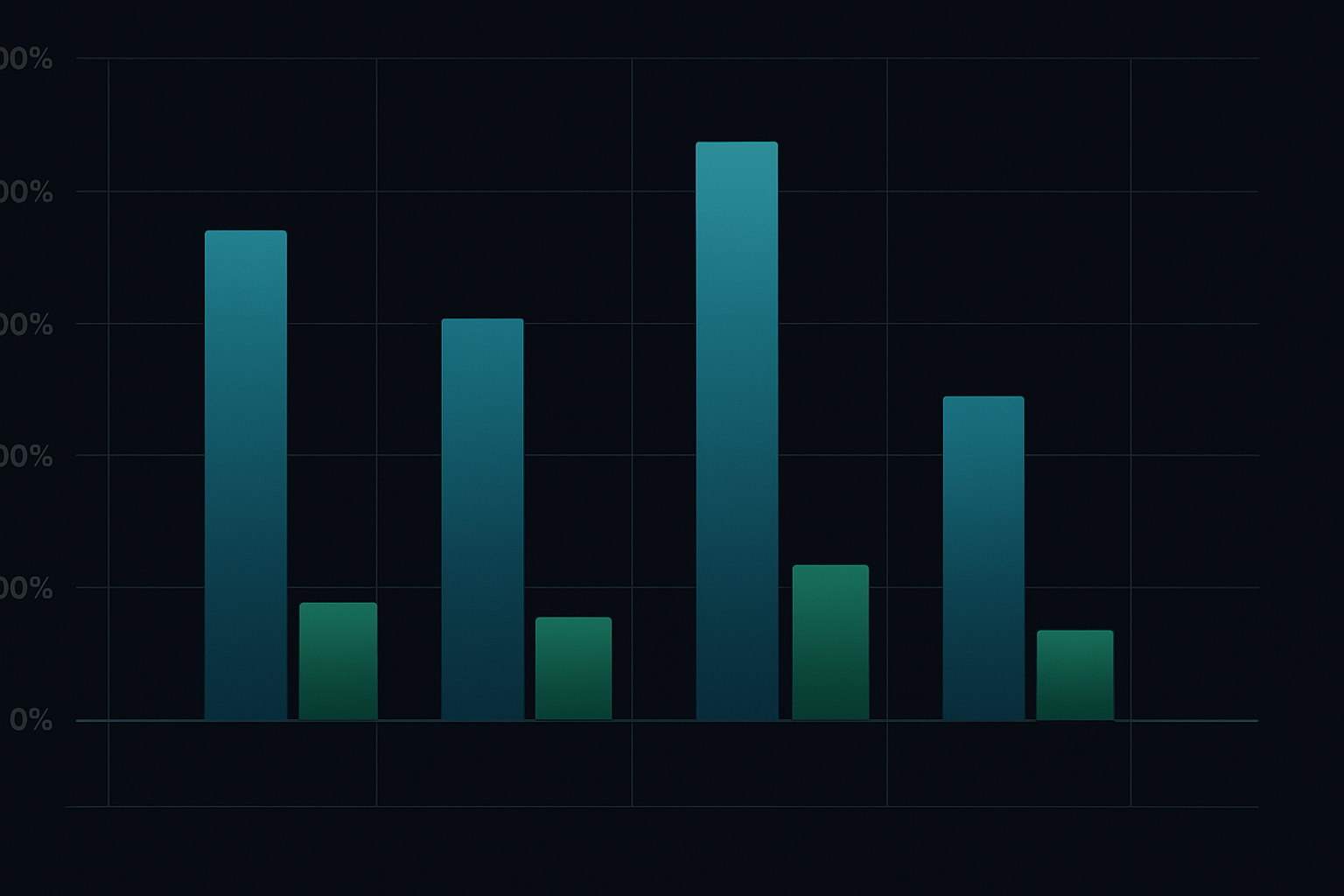

Brexit happened. The BoE slashed rates. Short Sterling futures exploded from 98.90 to 99.35. The butterfly paid maximum profit as volatility collapsed post-event. Return: 108% in three weeks.

Trade #2: The COVID Convergence (March 2020)

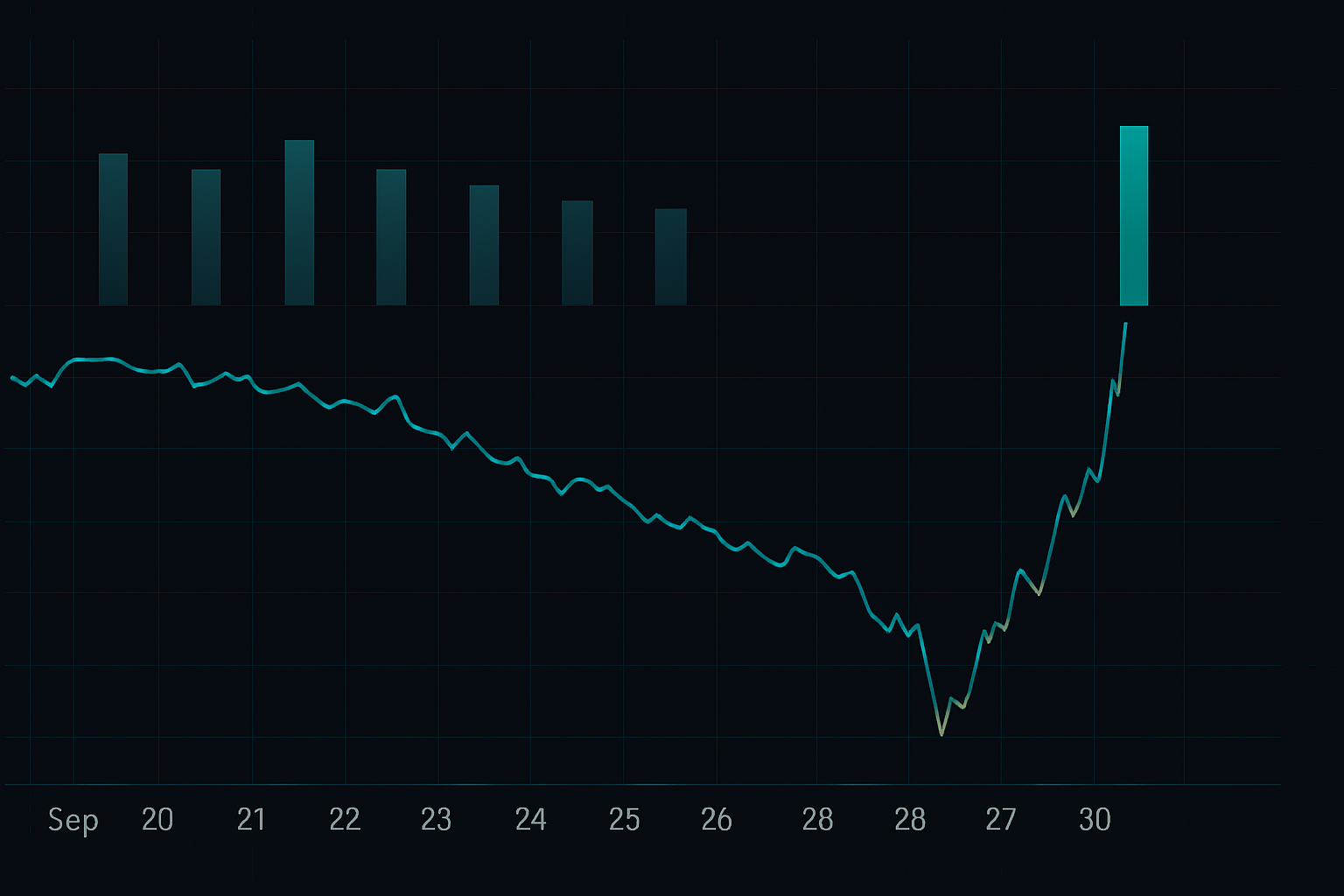

Fast forward to March 9, 2020. The Fed funds futures curve was still pricing gradual rate cuts over 12 months. Having seen this movie before during 2008, I knew the Fed would panic cut.

But instead of betting directionally, I played the curve convergence using calendar spreads in Fed funds futures:

- Long 10x June 2020 Fed funds at 98.75

- Short 10x December 2020 Fed funds at 99.25

- Spread: -50 basis points

The thesis: If the Fed panic cuts, the front months rally more than back months as cuts get front-loaded. Initial margin: $4,200 total.

March 15: Fed cuts to zero. June futures explode to 99.87. December futures only reach 99.90. Spread collapses from -50bp to -3bp. Profit: $11,750 on $4,200 margin. Return: 280%.

Trade #3: The Bank of England Pivot (September 2022)

The gilt market meltdown of September 2022 created the most violent rate derivative opportunity I've seen outside 2008. With UK pension funds getting margin called, the BoE had to pivot from hawkish to emergency QE in 48 hours.

On September 26, with SONIA futures pricing 6% rates by year-end, I structured this position:

- Buy 5x Dec22 95.00 SONIA calls at 2 ticks ($50 per contract)

- Buy 3x Mar23 95.50 SONIA calls at 5 ticks ($125 per contract)

- Total premium: $625

September 28: BoE announces emergency gilt purchases. Rate hike expectations collapse. Dec22 calls explode to 47 ticks. Mar23 calls hit 28 ticks. Exit: $3,675 profit on $625 risk. Return: 488%.

The Institutional Framework for Rate Derivative Trading

After executing hundreds of these trades, here's the framework that actually works:

1. Monitor the Divergence Signals

Look for divergence between cash rates, futures, and options markets. When options skew diverges from futures pricing, institutions are positioning for tail events. Track the 25-delta risk reversal in rate options - when it spikes, a policy shift is coming.

2. Structure for Asymmetry

Never bet directionally on rates. Use spreads, butterflies, and calendars to create asymmetric payoffs. The same risk management principles from equity options apply but with 10x leverage.

3. Size for Nuclear Moves

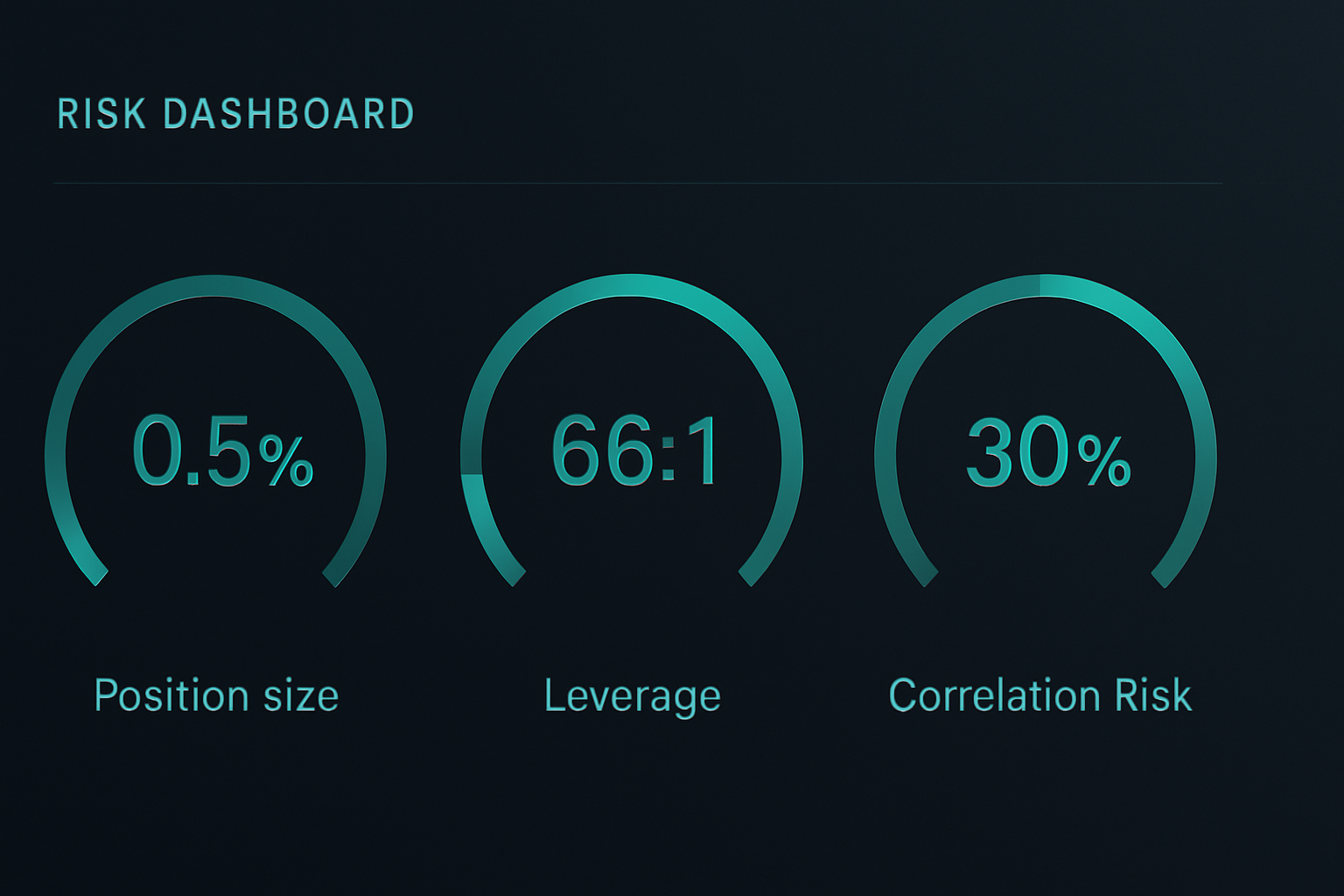

Rate derivatives can move 20-50x during policy shifts. Size positions assuming total loss, because when you're wrong, margin calls come fast. I never risk more than 0.5% of capital per rate derivative trade.

4. Trade the Aftermath

The best opportunities often come AFTER the initial policy response. Markets overshoot. In 2020, Eurodollar futures priced negative rates. Fading that extreme delivered 200%+ returns with less risk than catching the initial move.

Risk Management When Leverage Hits 100:1

Rate derivatives killed more prop traders at JPMorgan than any other product. Here's how to survive:

Position Sizing Math That Matters

With 66:1 futures leverage, a 15 basis point move against you doubles your margin requirement. Always calculate worst-case margin expansion. If a position can force liquidation before your stop, you're too big.

Use this formula: Maximum position size = Account equity / (Worst-case margin × 3)

The 3x buffer has saved me from every major rate shock since 2008.

The Stop Loss Paradox

Traditional stops don't work in rate derivatives. During fear market gaps, futures can gap 50 basis points overnight. Instead, use option hedges. Long an at-the-money put for every 5 futures contracts. It costs 10% of profits but prevents account destruction.

Correlation Bombs

When central banks move, correlations go to 1.0. Your Treasury futures, Eurodollar options, and SOFR spreads all move together. Never have more than 30% of risk in correlated rate positions. I learned this during the 2013 Taper Tantrum when every rate position moved against me simultaneously.

February 2026: The Next Rate Derivative Opportunity

Right now, with crypto in extreme fear and the broader market positioning defensively, rate markets are pricing something fascinating.

SOFR futures show zero rate cuts through June 2026. But the eurodollar option skew is screaming fear. The Apr26 96.50/97.00 call spread trades at 4 ticks - implying just 16% chance of rate cuts. Yet investment grade credit spreads have blown out 40 basis points this month.

This divergence matches the setup from March 2020. When credit markets scream while rate futures sleep, central banks act. The trade:

- Buy Jun26 SOFR 96.00/96.50 call spread at 8 ticks

- Risk: $200 per spread

- Maximum profit if SOFR futures > 96.50: $1,250

- Breakeven: Fed cuts just 42 basis points by June

With fear this extreme, one growth scare forces the Fed's hand. This spread offers 6:1 payoff on a 35% probability event.

The Reality of Rate Derivative Trading

Let me be clear: Rate derivatives aren't for everyone. They require understanding central bank reaction functions, curve dynamics, and institutional-grade risk management.

But if you're willing to put in the work, no other instrument offers similar leverage to policy shifts. While retail chases meme stocks and crypto pumps, institutions quietly position in rate derivatives before every major market turn.

The beauty is accessibility. You don't need a Bloomberg terminal. CME offers micro Treasury futures. CBOE lists retail-sized rate options. Even Interactive Brokers now offers SOFR futures to qualified accounts. Tools like FibAlgo's multi-timeframe analysis can help identify when rate market structure diverges from price action.

Start small. Paper trade through one Fed meeting. Track how different contracts react. Build intuition for how policy expectations translate to derivative prices.

Because when the next crisis hits - and it will - central banks will slash rates faster than markets expect. And if you're positioned correctly in rate derivatives, that 500% return opportunity will be there.

Just remember: The same leverage that creates those returns can destroy accounts even faster. Never trade rate derivatives without accepting you could lose everything you risk. But for those who master the instrument, it's the most powerful tool in finance during fear markets.